Debunking the 3 Most Common Myths About the 2023 Housing Market

Constantly changing headlines and predictions make the 2023 housing market extremely challenging to navigate. Unfortunately, the number of misconceptions about buying, selling and owning a home has never been higher. According to a recent survey by Fannie Mae, 82% of people believe it’s a bad time to buy a home.

We’ve always known there is a lot of fear and uncertainty around the housing market, but we were reminded of this in a big way recently after one of our team mates posted a video on Instagram talking about how home prices will be affected when interest rates come down.

Comments flooded in, most of which were quite negative about future housing demand and the stability of home prices in the face of a looming recession. Most of the comments argued these three points:

- Mortgage rates are not going to come down.

- Even if mortgage rates do come down, nobody is going to buy homes because prices are too high.

- Home prices are falling and will continue to fall.

We understand the headlines can sometimes be alarming: “Home sales activity at a decade low.” “Prices are collapsing.” “The market is set to crash.” The attention-grabbing narratives can be confusing to those who are reading that the market is in trouble, yet finding very competitive conditions and price increases when they look at homes. With so many competing voices vying for your attention – who do you trust?

As mortgage advisors, the biggest part of our job today is dispelling myths like those listed above. In this article, we’ll break down the FACTS and DATA about what’s currently going on with supply and demand, what has happened in the past with home prices and interest rates, and what we believe will happen in the future.

Myth #1: Interest rates are not going to come down.

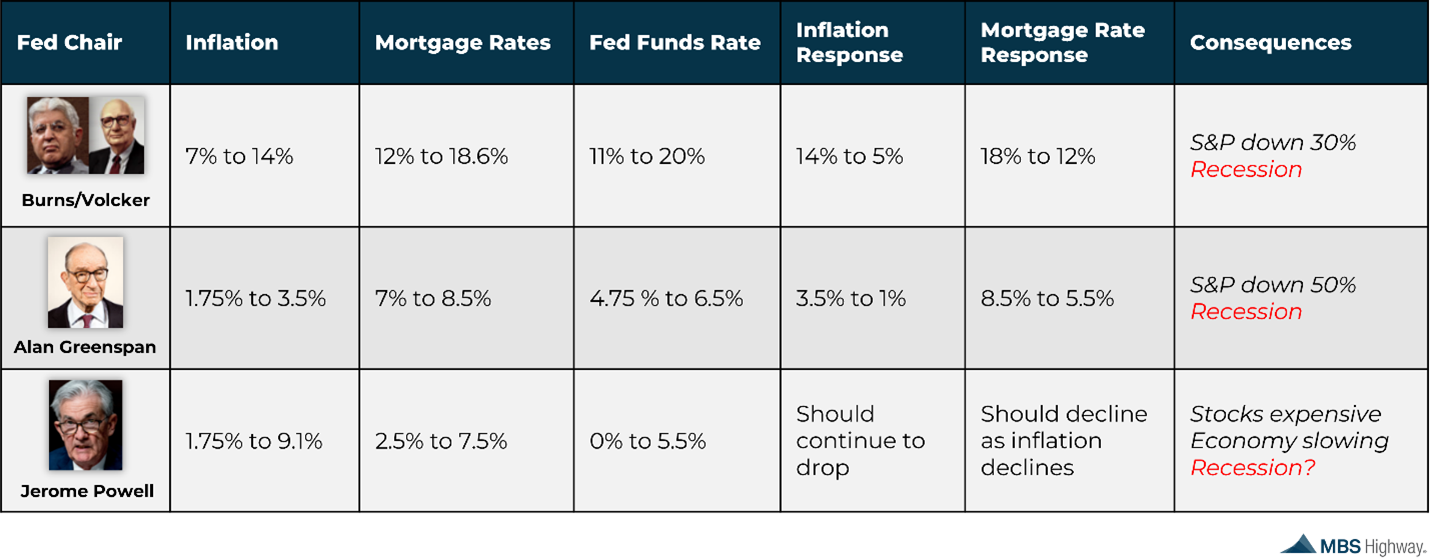

Let’s look at the history of the Federal Reserve’s economic policy, recessions, and their impact on mortgage rates.

In the early 1980s, tight monetary policy in the United States to control inflation led to a recession. The Fed Funds rate was increased from 11% to 20% to combat the hyperinflation that carried over from the 70s because of the 1973 oil crisis and the 1979 energy crisis.

In the two years leading up to this recession, fixed mortgage rates reached their highest point in modern history at an annual average of 18.6%. However, once inflation calmed down and the recession started, rates fell to 12%.

In 1994, the Federal Reserve began a tightening program to proactively prevent inflation that they saw on the horizon. This cycle saw interest rates rise by nearly 3% in a little over 12 months, and mortgage rates jump 1.5%. Inflation fell as a result and a recession was actually avoided. The market response saw mortgage rates drop even lower than they had been previously down to 5.5%.

This brings us to the current monetary tightening cycle. In the last 3 years, we’ve seen inflation jump from 1.75% to 9.1%. Consequently, mortgage rates skyrocketed from a low of 2.5% to a high of over 7%.

The Federal Reserve has hiked the Fed Funds rate at the fastest pace in history, up to 5.33% currently. This aggressive monetary policy will eventually bring inflation down and push the economy into a recession, which will bode well for mortgage rates.

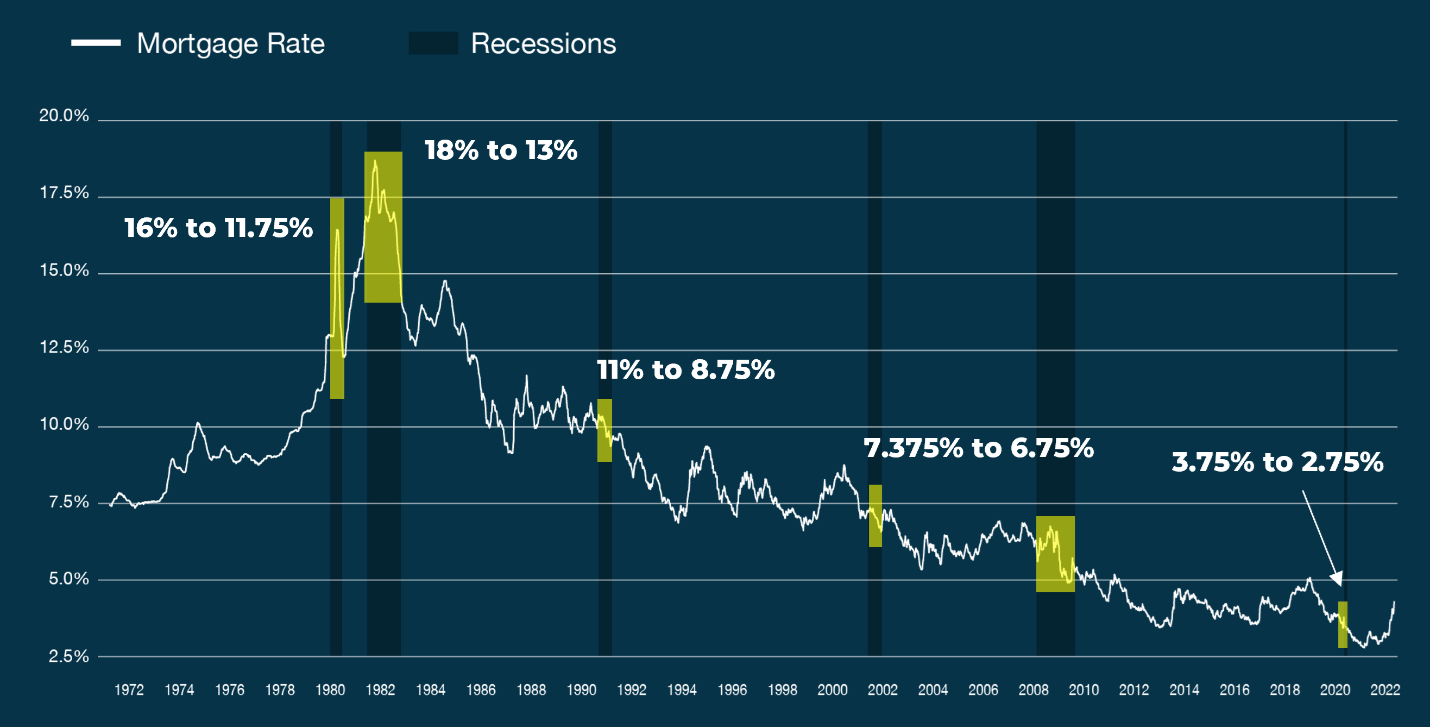

We know this will be good news for rates by looking at how they have responded during previous recessions. As you can see in the graph below, mortgage rates have decreased either during or immediately following each of the last six U.S. recessions.

Myth #2: Lower mortgage rates will not bring more buyers into the market.

A lot of people think that, even if mortgage rates do come down, nobody is going to buy homes because prices are too high.

Prices of course have an effect on home affordability, but so do interest rates. Rates will come down eventually, and even a small decrease will impact affordability in a meaningful way. For every 0.5% improvement in interest rate, the payment on a median priced home (currently $416,1000) decreases roughly $110.

According to realtor.com, when mortgage rates push 7%, 20 million households are priced out of the market compared to when rates are at 3%. Essentially, this means that for every 1% drop in mortgage rates, 5 million more borrowers are able to afford a mortgage on a median priced home.

In order to have that same impact on affordability, the value of the median priced home would have to decrease by almost 11%. And there is just no concrete evidence that this is going to happen (more on that below).

Lower prices could also have an opposite effect when it comes to buyer demand. Currently, there are a lot of homeowners who want to move but do not want to give up their low interest rate. If home prices come down before interest rates do, these homeowners will be even more entrenched in their homes because they will not want to sell at a lower price.

Myth #3: Home prices are falling and will continue to fall.

Those who think home prices are falling simply are not paying attention.

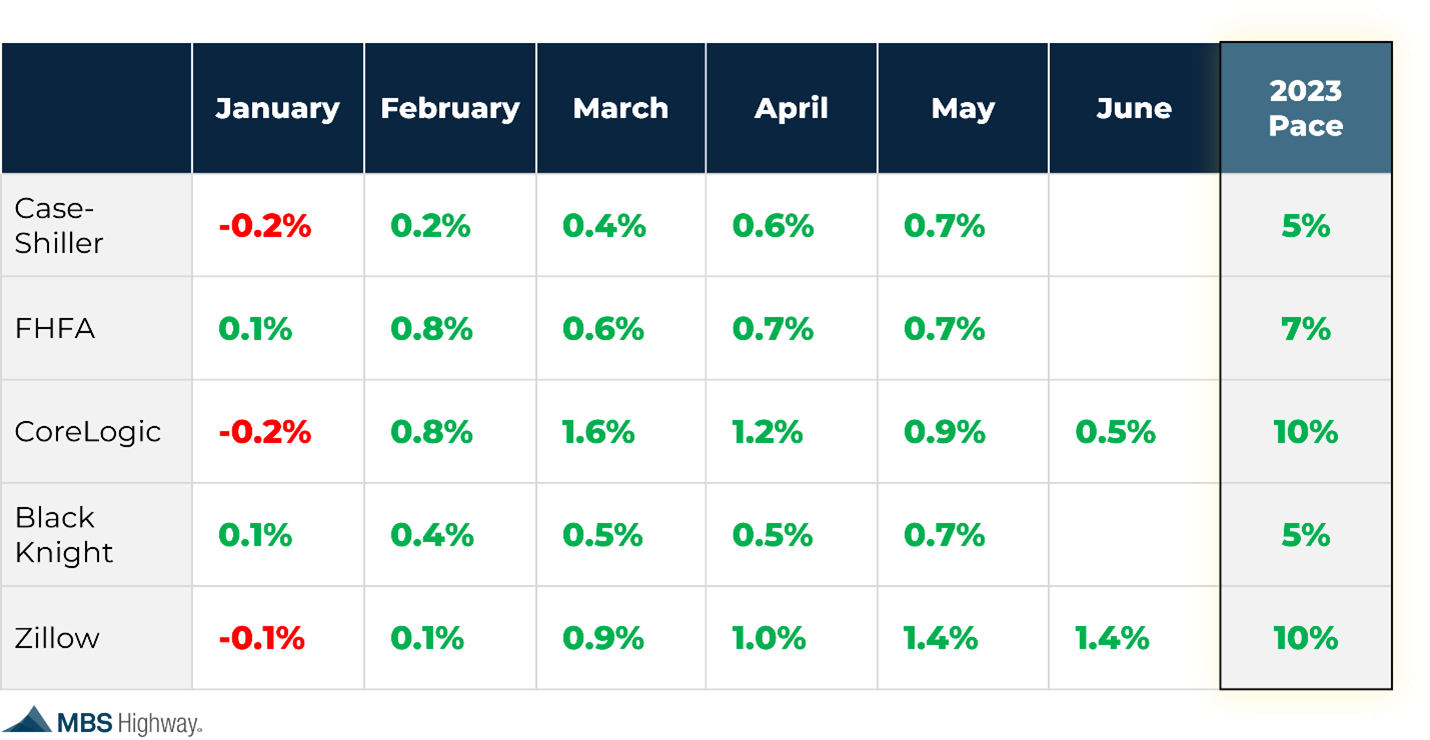

Home prices reversed course in February have stayed that way. All of the reputable home price indexes confirm that in many areas of the country, price cooldowns were just mild corrections. Not only that, but many of the new numbers have eclipsed the ones we saw at the peak of the market in June of 2022.

According to Black Knight’s August 2023 Mortgage Monitor report, prices have now reached new peaks in 30 of the 50 largest markets, with several northeastern metros currently 5-8% above their 2022 highs.

Goldman Sachs housing analysts also recently changed their tune on the market and no longer think home prices will fall this year. Instead, they are forecasting a slight increase.

We are revising our home price forecasts higher, to 1.8% for full-year 2023 vs. -2.2% prior, and 3.5% in 2024 vs. 2.8% prior,” Vinay Viswanathan, a fixed income strategist at Goldman Sachs, wrote in a note for the firm’s housing team. “These forecasts imply home prices will remain roughly unchanged through [the] year-end and then return to trend growth levels in 2024.

The reason home prices will continue to rise is because there are still not enough homes on the market. According to Black Knight’s report, inventory has declined in 95% of the major U.S. housing markets since the start of 2023.

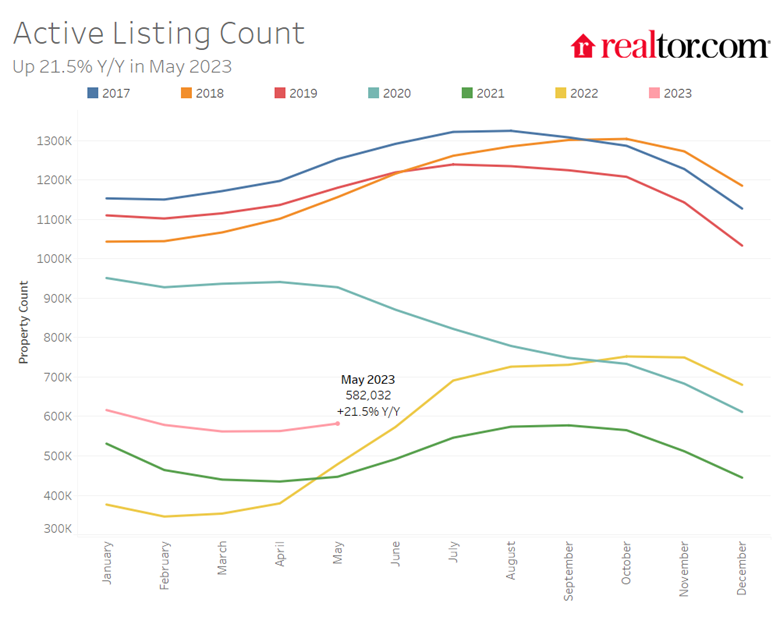

Realtor.com’s July housing data draws the same conclusion. While we are still seeing a small amount of month-over-month growth in active listings (a spike happens every year around this time), the growth rate is declining as sellers continue to list fewer homes than last year and buyers compete over the remaining affordable homes for sale.

As you can see below, while inventory has increased since last year, it is still drastically lower than at the start of the pandemic.

The Bottom Line

Home prices are determined by two things: supply and demand. Yes, there are few buyers in an inflation-heavy economy with high interest rates, but in order for home prices to go down there needs to be fewer buyers than sellers – and that is just not within the realm of possibility today.

There is a lot of pent up demand in the housing market right now that has been kept at bay because of the affordability problem. But as affordability improves, we are going to continue to see more people move forward with their homebuying plans.